Before you sign anything.

When the phone starts ringing

Certain seasons of life invite certain kinds of advice. A spouse dies, and the phone begins ringing with condolences from financial professionals. A marriage ends, and someone suggests you roll your settlement into a managed account before you have finished grieving. A business you spent thirty years building finally sells, and within weeks someone is explaining an annuity that guarantees income for life. An inheritance lands, and three different family members tell you three different things to do with it.

What these moments share is urgency. People around you — often with good intentions, sometimes without, begin asking you to make permanent decisions at the moment you are least equipped to make them.

What the research says

13.7% of recent widows had fired or changed their advisors within a year of their spouse’s death — not because markets moved against them, but because the relationship was never really theirs, and because someone began selling to them the week the funeral ended. Divorced women report the same thing. People who inherit suddenly describe a flood of advice from professionals who benefit from their decisions.

Mainstream financial-education sources — the Consumer Financial Protection Bureau, FINRA, Britannica Money — publicly warn the recently widowed about high-pressure product sales. Several of them specifically recommend getting a second opinion before signing any annuity, long-term care policy, or other expensive financial product being sold during grief.

The question is where that second opinion is supposed to come from. The industry is organized around selling things. Most second opinions arrive from someone who happens to have a slightly different product to pitch.

A second opinion that isn't selling something else

Clear View Financial exists for exactly this moment. Kevin Dingle, the founder, is a financial clarity coach. He does not sell insurance, annuities, or managed investment products. He is not paid more if you buy one thing over another, because he is not paid for that at all. He is paid a flat fee for the time you spend with him — nothing beyond it.

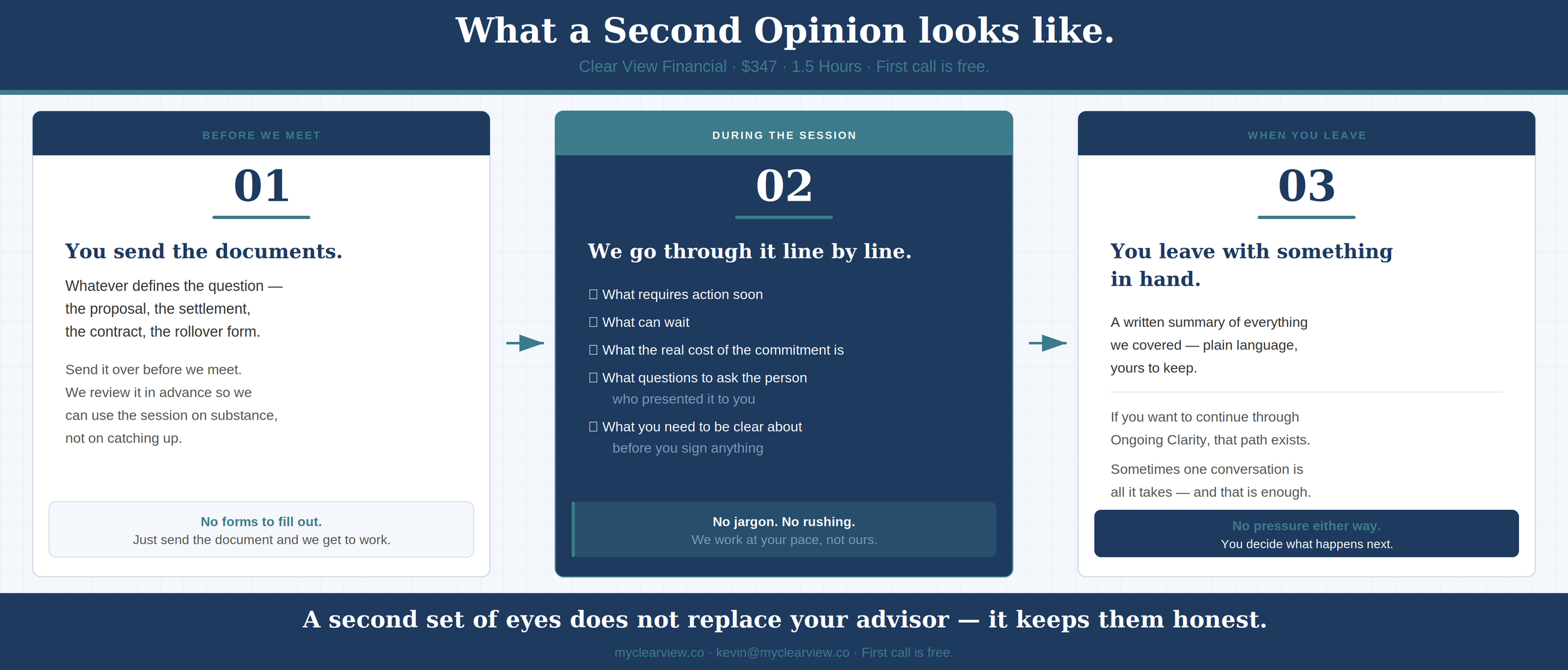

Bring the contract. Bring the proposal. Bring the statements, the spreadsheet your brother-in-law sent you, the business-sale paperwork you do not fully understand. In ninety minutes, we go through what the document actually says — the fees, the commitments, the language that matters, the language that is missing — so you can walk into your next conversation knowing exactly what you are being asked to agree to.

Clear View Financial Services is a financial coaching practice. We do not sell financial products, manage assets, or recommend specific securities. All conversations are confidential, no information is shared with any outside party. All conversations are confidential. Clear View Financial is not a Certified Divorce Financial Analyst.